Are You Prepared For The Next Recession?

There has been a lot of talk about a possible economic recession in the news lately. This makes people nervous as most of us remember what it was like during the Great Recession that occurred from 2007 to 2009. People lost their savings, their homes, and their jobs. No one wants to live through the pain of that again. A Recession just like economic expansions are inevitable part of the economic business cycle. The question for us is how can we make sure we are properly prepared financially for the next recession?

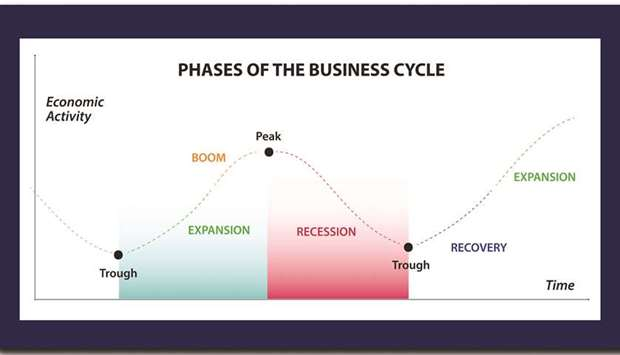

The Business Cycle

Before we can talk about a recession, it is good to have a general understanding of the Economic Business Cycle. The Business Cycle is the natural “life span” of an economic period. All business cycles are characterized by several different stages, as seen below.

1. Expansion

There is an increase in employment, incomes, production, and sales. Debt is low and investments are high in an expansion.

2. Peak

The peak is reached at the height of the business cycle. The economy begins to stall as it has reached the maximum level of growth. People begin to adjust their lifestyle and expenses due to high prices and inflation.

3. Recession

These are periods of contraction. During a recession, unemployment rises, production slows down, sales start to drop because of a decline in demand, and incomes become stagnant or decline. Recessions go hand-in-hand with a “Bear” Stock Market (When stocks fall more than 20% from its 52 week high).

4. Trough

This period marks the end of the recession and an economy begins moving into the next step: recovery.

5. Recovery

In this stage, the economy starts to turn around. Low prices spur an increase in demand, employment and production start to rise, and lenders start to open up their credit coffers. This stage marks the end of one business cycle.

Where are we now in the business cycle?

The Great Recession ended in in mid-June 2009 and the U.S. Economy has been expanding ever since. The current 10-year expansion is the longest in U.S. history. However, recent events like the seemingly never-ending trade war with China, a slowing down of the global economy, and an inverted bond yield curve (short term interest rates are higher than long term interest rates) are warning signs that the U.S. Economy is at its peak and headed towards a recession.

How will we know if we are in a recession?

What exactly is an economic recession and how do we know when we are in one? A recession occurs when there is a decline in one or more of the following economic indicators for at least 6 months:

- Real Gross Domestic Product

- Income

- Employment

- Manufacturing

- Retail Sales

The National Bureau of Economic Research (NBER), a private non-profit group whose board includes economic leaders and Nobel Prize winners. The NBER analyzes the economic data and they make the official announcement of when a recession begins and ends.

The difficult thing about a recession is that we could be in one and not yet even know it. That is because it takes at least 6 months to analyze the economic data before an official announcement comes out. However, the symptoms of a recession, like a bad cold or flu, can be felt before it actually hits you. It starts out like a sniffle, then a cough, then a headache, then chills. All of a sudden you are bed ridden for a few days; or worse you have to see the doctor because you have the flu.

The Great Recession of 2008 started off like a possible cold than turned into a severe economic flu. The housing market began to slowdown and many believed this was just a sign that the housing bubble was going to burst. However, this led to the Subprime Mortgage Crisis. This led to the collapse of a number of major investment banks including Bear Stearns and Lehman Brothers. This in turn led to a severe decline in the U.S. Stock Market, a global financial crisis, a rise in bankruptcies, and severe unemployment.

Since the Great Depression we have had 13 recessions. The Great Recession lasted 1 ½ years. Other recessions lasted anywhere from 6 months to 1 year and 4 months. While the duration might not be long, the impact to consumers can be significant. It could lead to a loss of a job, a home, income, and investments.

6 Tips to help protect you in the next recession

Given the potential severity that a recession can cause, what can you do to protect yourselves and your family from the impact of the next recession?

1. Make sure you have job security

In a recession, companies might be forced to layoff employees. How secure are you in your position? Take steps to ensure that your skills are relevant to your employer and you are continually demonstrating your value. Just in case, make sure your resume is up to date and keep up to date with the people and trends in your profession. (Make sure you have a good LinkedIn profile and a solid list of connections within your industry)

2. Have a sufficient emergency fund in place

Do you have enough money saved in case you lose your job? At a basic level you should have enough cash to pay your household expenses for 3 to 6 months. If you have a home, you should increase that cash savings to 12 to 24 months of expenses. It might take you that long to find a new job if you are laid off in a recession and you want to make sure you can pay your mortgage payments. In an economic downturn, the last thing you want to do is to tap your 401K plan as they have likely declined in value. If you take money out, it will take you even more time and money to replenish your 401K to a level that will meet your retirement needs.

3. Minimize your debts

In an economic downturn you will probably need to reduce your expenses especially if you have a reduction in income or a loss of a job. Having to pay off credit card debt at the same time will be a drag and limit your ability to spend your income on the things you need most. Now is the time to pay off your credit cards and make sure you pay them off in full each month.

4. Take a close look at how much stocks you own

What percentage of your investments are in stocks and will you be relying on that money soon? If you are 1 to 2 years from your retirement date you should take a close look at your 401K and other investments you are relying on for retirement and make sure money you need for the first few years of retirement are not overly exposed in stocks. You do not want a sudden decline in the value of your 401K just when you will begin taking money out of it.

5. Diversify your investment portfolio

The Stock Market by nature is volatile (it goes up and down). In a recession that volatility is heightened considerably. To dampen this volatility, invest globally in stocks, bonds, and cash. Also make sure your mix of these investments matches your risk tolerance (appetite for losses) and time horizon (when will you need to withdraw money from your investments).

6. Don’t Make Hasty Investment Decisions

As I mentioned above, recessions while painful, they do not last forever. Your investments will lose money during a recession. It is important to know that they also go back up after the recession ends. As the chart below indicates, over time, the Markets have rewarded investors who stay disciplined, focused, and do not stray from their long-term investment strategy.

_______________________________________________________________________________________

This content is developed from sources believed to be providing accurate information, and provided by Attune Financial Planning. Please consult your financial, legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information only.